Two years ago WaterOne in Johnson County made a deal with the devil…

Two years ago WaterOne in Johnson County made a deal with the devil…

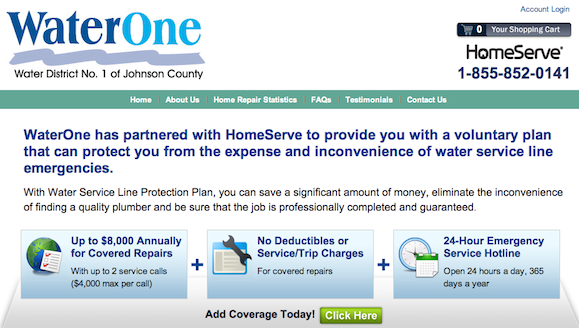

The utility agreed to allow HomeServe – a 20 year-old British plumbing repair and insurance company – to hawk its wares using the local water company’s letterhead and website to sell pipe protection insurance policies to locals.

“WaterOne has partnered with HomeServe to provide you with a voluntary plan that can protect you from the expense and inconvenience of water service line emergencies,” reads the pitch on WaterOne’s website. “With the Water Service Line Protection Plan, you can save a significant amount of money, eliminate the line inconvenience of finding a quality plumber and be sure that the job is professionally completed and guaranteed.”

In return for allowing HomeServe to trade on WaterOne’s good name – resulting in significantly more sales – the local water company gets a kickback or commission from the Walsall, England based firm.

The $64 million question being, is it a good deal for homeowners and will HomeServe be around to cover their claims in the years to come?

The Better Business Bureau has its doubts.

“BBB encourages caution as HomeServe USA solicits locally,” reads a headline on the bureau’s website. “BBB has received numerous complaints, from consumers across the country, concerning this business’s direct mail solicitations, specifically that the solicitations’ layout may cause consumers to perceive the letters as coming from the consumers’ utility companies and not an independent business selling home warranty or insurance coverage.

“BBB also received customer complaints concerning coverage issues, specifically that when a problem occured, it was not covered by the policy.”

Therein lies the problem.

While WaterOne’s website and mailings say that it’s “partnered” with HomeServe, the implication to consumers is that WaterOne is backing the repairs, which is not the case.

Take a look at the dictionary definition of the word partnered:

Take a look at the dictionary definition of the word partnered:

“A person associated with another or others as a principal or a contributor of capital in a business or joint venture, usually sharing its risks and profits.”

While WaterOne is sharing in the profits from these sales – HomeServe, not WaterOne – is the only one on the line for any homeowner claims.

In other words, WaterOne does not stand behind the policies.

Roger the Plumber‘s take:

Roger the Plumber‘s take:

“I think the water line insurance is not a good deal,” he says. “Because if you’ve got a copper water line coming in it’s going to last 150 years. And it’s going to be rare that they have a water line claim because most of the water lines in Johnson County went out in the 1970s and have been replaced. It’s very rare that we see a water line claim anymore.

“They’ll clean up on the water line insurance, they’ll flat clean up,” Roger adds. “Because in addition to the repairs being unlikely, they aren’t that expensive to replace.”

So can HomeServe pay for and provide the repairs?

HomeServe USA is merely a division of the parent company in England, a company that based on recent reports is experiencing serious difficulties.

“HOMESERVE, the boiler repair company, is struggling with an emergency of its own as it continues to leak customers in the core UK business, a trading update revealed yesterday,” London’s Telegraph reported September 30th.

“As the company heads into a crucial six-month period, during which customers decide whether or not to renew their contracts, the shares are looking decidedly shaky, with the group still labouring under an investigation from the Financial Conduct Authority.

“Homeserve, which sells products such as boiler repair cover and plumbing and drainage insurance, built its stock market reputation on pleasing investors with rapid growth rates driven by a slick marketing machine that attracted thousands of customers.

“But this all came to an abrupt halt when it suspended all of its telesales and marketing activities in October 2011 following an internal review by accounting firm Deloitte that discovered sales practices that the company said at the time ‘did not meet the company’s high standards.’ ”

As for hawking its sewer service here in Johnson County, “I think the only way they’d be able to sell these plans is because of the endorsement of (WaterOne),” Roger says. “But we don’t know who is going to do the repairs or if they’re going to cut corners and just do repairs instead of replacement. Most of the time when you’re having a sewer problem it should be replaced, not repaired.”

Here’s how HomeServe USA’s game is being played out here:

Here’s how HomeServe USA’s game is being played out here:

“(It’s) a marketing strategy by a private company that uses a city’s logo on a letter, above the mayor’s name, to get its pitch before potential customers,” the Star’s Matt Campbell reported two years back. “It works. More than 12 percent of 7,800 households in Prairie Village that received that letter recently have signed up, according to Dennis Enslinger, assistant city administrator. City Hall, in return, gets a 10 percent cut of the premiums.”

Will the company – or more to the point – its US division be around to pick up the tab if and when consumers make claims? We’ll see, but there’s room for concern the Telegraph reports.

“HomeServe has some bright spots such as growth in the US and a stable business in France but, as previously illustrated, these aren’t big enough to offset any hole the UK business will leave.”

As for the Better Business Bureau findings, “HomeServe USA is headquartered in Stamford, CT.,” the agency says. “BBB|Connecticut rated the company a D, on an A+ to F scale, and noted that HomeServe USA has entered into consent agreements with the states of Kentucky, Ohio and Massachusetts. Both Kentucky and Ohio alleged that the mailing solicitations ‘generated confusion’ and were ‘deceptive’ in their appearance. According to the BBB Business Review, the settlements should not be considered as an admission of guilt or a legal violation.”

Stay tuned.

Most homeowner’s can buy a rider to their homeowner’s coverage to take care of these type of expenses, both coming in and going out, at about half what the limey’s want.

sorry Karl, not true. The HO policy is intended to cover only the structure and is pretty limited with regards to even the foundation. Once that pipe leaves the structure/foundation/basement, you are on your own. If your agent told you otherwise, he/she is wrong.

Sorry I pay the bill monthly and State Farm takes the money, same with earthquake coverage. It shows in the rider section of my policy as does my over limit liability coverage.

hmmm, thanks for the info. I’ll share that info with the carriers I represent. I’ve been selling HO policies for about 40 years and represented dozens of companies. Not a one has ever offered and the standard policy form clearly excludes. I do carry the earthquake but that coverage has a pretty substantial deductible. Water back-up is a common endorsement and you can get flood but never heard of coverage for pipes once they leave the structure. Thanks for the heads up. I will contact the State Farm claims department for a clarification. I’m guessing you confirmed with State Farms claim adjustor before signing Not to trash my peers but a healthy number of insurance salesmen are about as trustworthy as car salesmen. Always get an honest answer from the claims dept. as opposed to what the agent will tell you. Thanks again.

Ks. Karl; Just got off the phone with the SF claims people. They advised they do not cover pipes once they leave the structure. I’d say call your agent and then the claims dept. directly.

Excellent topic and well researched. I have gotten the mailers, initially from WaterOne and a few times since then from Home Serve directly. My recollection is that WaterOne did make clear, at least to me, that if and when an issue arose where I needed service as a result of a break, I would be dealing with and only with the vendor. I do agree that they are clearly benefiting from being linked with WaterOne. While I never pulled the trigger on securing the coverage, I always wondered what the likelihood of a break where I needed the service. Getting Roger the Plumbers opinion makes me much more confident in my decision to not spend the money.

Good stuff HC !!!

This is the kind of news we need more of. Good work!

HC, you should get the opinion of the County Commissioners on this one. Commissioners Eilert and Peterson are going to run against each other for the Chairman of the Board. They are already throwing barbs.

When at United Telecom, prior to moving to the Sprint side, I had an alarmingly similar experience. Telecom deregulation had just taken place, leaving the telco’s responsibility ending at the demarcation, typically the “phone company” box attached to the outside of your house.

I developed a program to insure the inside wire, previously installed by the telco. If anything happened to the phone wiring, post dereg, you would have been out $60/hr to search out and repair the problem as we no longer owned that wire, it was passed to the homeowner. I don’t remember for sure, but the cost was something like a $1.50 on the bill, monthly. If you had a problem inside the house, we fixed it for free if you signed up.

I ran the program by all the concerned Public Utility Commissions, out of courtesy, since it was not in their purview, but they had a lot of control over us so I just wanted to do a casual presentation and get their blessing.

I sent a notice to each and every customer for 3 months straight, explaining the program. On the 3rd month, I included what’s called a “negative ballot”, much like the procedure used by people like Columbia Record Club; sign the card and send it in if you want to OPT OUT, otherwise, we will bill you staring on the 4th month.

I covered every base possible, internally and externally. We knew it would have a backlash but not one we could really measure. Outcome; it became the only story Stan Kramer did for THREE NIGHTS IN A ROW on his “Call for Action Hot Line!”

Just as our PR/damage control firm told us, it would blow over in days, and it did. It went on to be a huge benefit to the clients who signed up, or didn’t, and was one of the highest margin products I’d developed.

It all depends on how you look at it.

When I got this, I called up City Hall for information and they directed me to someone at the Water District. After several more attempts, I finally spoke to someone who had an opinion as to what type of pipe I might have in my front yard. He said, despite what Roger said, that with older homes, you have no idea what the pipe is made of. It could be old corroded pipes by now. there were no codes in the 50s and builders could have used very cheap pipe material. He thought the insurance was cheap compared to the potential costs.

I certainly realized, by carefully reading the mailer, that this company was solely responsible for repairs. I am not concerned about “deceptive” sales practices. I am concerned that they will be in business if something happens.

A friend’s neighbor in PV had their pipes break and the cost was maybe $10K. Pretty cheap insurance.

A better article would focus on their accountant who rang an alarm in 2010 and a followup on that to see if those problems have been resolved.

Don’t forget the Better Business Bureau part about them not honoring claims. Read the policy closely before you jump. Apparently there are a number of things the homeowner must do before the insurance becomes valid. As in before the company will pay off.

And as I recall, $10,000 is more than double the maximum this insurance will cover.

Eh, if mine busts I’ll just rent a backhoe and run copper tubing from the shutoff to the meter, I already have access to the shutoff. Waste of money for me.

Jokes on the city of PV, I poop in a dry RV toilet and use the grey water for my tomatoes!

Hello everyone. Rodger The Plumber is the BOMB! Every part in his truck for everything. Love it. His kid was in my troop as a kid so he was involved too. Way involved! Nice guy!

Ok, this is coverage for the FRESH water line and not the SEWER line. The article quotes RTP as saying “”Most of the time when you’re having a sewer problem it should be replaced, not repaired.”” This has nothing to do with the sewer line so wanted to get this cleared up. Sewer lines do F up very badly in post war era homes in NE Johnson County. This is because of tree roots getting through joints where the older pipes were pushed together. My next door neighbor’s completely collapsed and they had to REPLACE the entire run to the main. He is correct that they need to replace the entire thing. HO insurance did not cover this for her and it was very expensive. Copper sulfate root killer twice a year is the rule in Brother Sunday’s house.

I was told by a State Farm agent that they do NOT cover the outside sewer line.

She also advised me that there were companies that took care of this but much of

the cost is not covered. I had Anthony Plumbing come out several times and also a handyman come in to unclog the line. Anthony Plumbing took pictures of the line

and showed them to me but I didn’t get a copy of the photos, or a written description

The inside of the pipes looked kinda rough, which they pointed out and said tissues would catch on the pipe and build up. They said replacement could run me Est.$18,000. OR, I could have the do a power wash type of cleaning and that could last me up to 5 years. I am a window, elderly and handicapped and dicided to do the power wash because I believe this house is too, big for me to continue to care for. Wish about 5 years ago when I asked my agent about this I could have found a reliable insurance company. However, I believed my agent and that the coverage wasn’t worth it.